N-MFP: Parse Money Market Fund Filings with Python

Money market funds file Form N-MFP monthly to report their complete portfolios, yields, net asset values, and liquidity metrics. EdgarTools parses both N-MFP3 (June 2024+) and N-MFP2 (2010–mid 2024) filings into structured Python objects.

from edgar import get_filings

filings = get_filings(form="N-MFP3")

mmf = filings[0].obj()

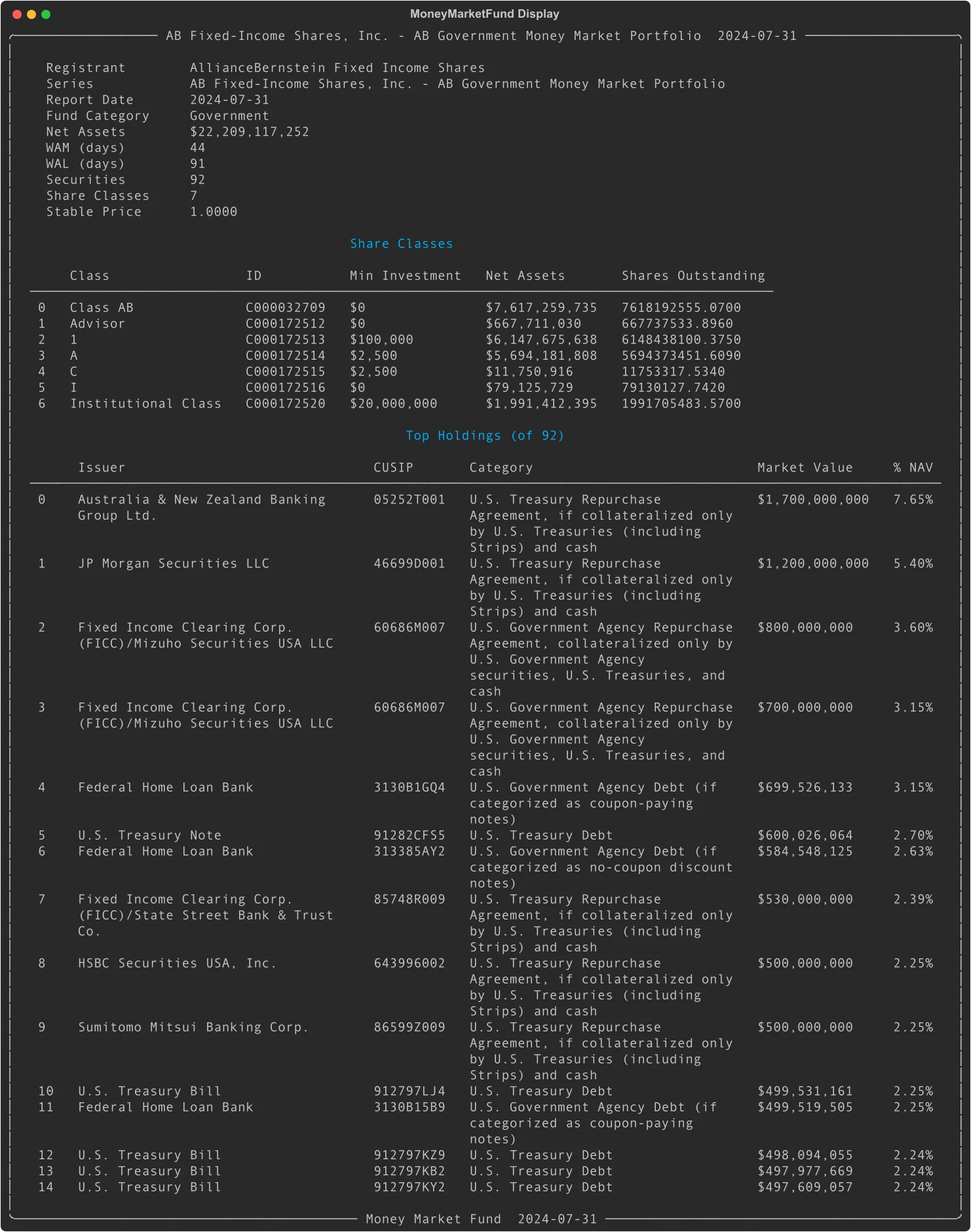

mmf

Three lines to get a fully parsed money market fund report with net assets, weighted average maturity, portfolio holdings, and share class details.

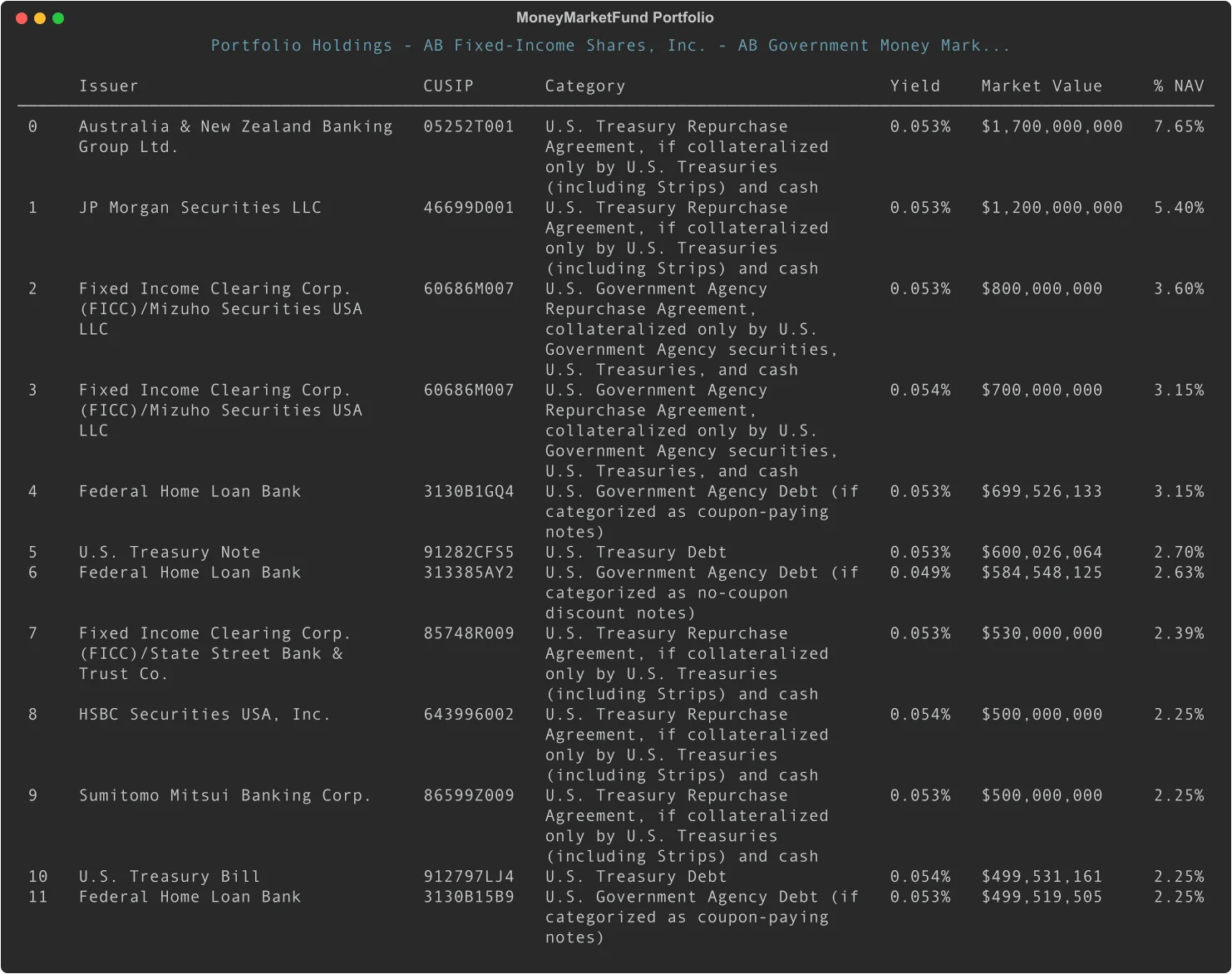

Portfolio Holdings

The portfolio_data() method returns a DataFrame with every security in the fund, sorted by market value:

mmf.portfolio_data()

| Column | What it is |

|---|---|

issuer |

Issuer name ("U.S. Treasury") |

title |

Security title ("T-Bill") |

cusip |

9-character CUSIP |

isin |

ISIN identifier |

category |

Investment category ("TreasuryDebt", "CommPaper", etc.) |

maturity_wam |

Maturity date for WAM calculation |

maturity_wal |

Maturity date for WAL calculation |

yield |

Yield rate as decimal |

market_value |

Market value in full dollars |

amortized_cost |

Amortized cost in full dollars |

pct_of_nav |

Percentage of net asset value |

daily_liquid |

Daily liquid asset flag |

weekly_liquid |

Weekly liquid asset flag |

has_repo |

Has repurchase agreement collateral |

Market values are in full dollars -- not thousands. A market_value of 5,000,000,000 means exactly $5 billion.

Repurchase Agreement Collateral

Money market funds often hold repurchase agreements secured by government or agency securities. The collateral_data() method flattens all repo collateral into a single DataFrame:

mmf.collateral_data()

| Column | What it is |

|---|---|

security_issuer |

The repo counterparty |

security_cusip |

CUSIP of the repo agreement |

collateral_issuer |

Issuer of the collateral security |

collateral_cusip |

CUSIP of the collateral |

collateral_lei |

LEI of collateral issuer |

maturity_date |

Collateral maturity date |

coupon |

Collateral coupon rate |

principal_amount |

Principal amount of collateral |

collateral_value |

Market value of collateral |

collateral_category |

Type of collateral security |

This is useful for analyzing the credit quality and composition of repo collateral backing the fund's assets.

Share Class Information

Money market funds typically offer multiple share classes with different expense structures and minimum investments. Access share class details with:

mmf.share_class_data()

| Column | What it is |

|---|---|

class_name |

Share class name ("Class A", "Institutional") |

class_id |

SEC series identifier |

min_investment |

Minimum initial investment |

net_assets |

Net assets for this share class |

shares_outstanding |

Total shares outstanding |

Yield and NAV Time Series

N-MFP3 (June 2024+): Daily Time Series

N-MFP3 filings include 20 days of daily data for yields, NAV, and liquidity metrics.

# 7-day gross yield history (series-level)

mmf.yield_history()

# Daily NAV per share history (series-level)

mmf.nav_history()

# Daily and weekly liquid asset percentages

mmf.liquidity_history()

Each method returns a DataFrame with a date column and the corresponding metric values.

Yield history shows the 7-day gross yield over the reporting period. NAV history tracks daily NAV per share. Liquidity history shows both daily liquid assets (securities that can convert to cash in 1 business day) and weekly liquid assets (convertible within 5 business days), reported as both dollar amounts and percentages of net assets.

N-MFP2 (2010–mid 2024): Weekly Snapshots

N-MFP2 filings report weekly Friday snapshots instead of daily time series. The same methods work, but the date column uses labels like "week_1", "week_2", etc., and yields are single scalar values rather than a time series.

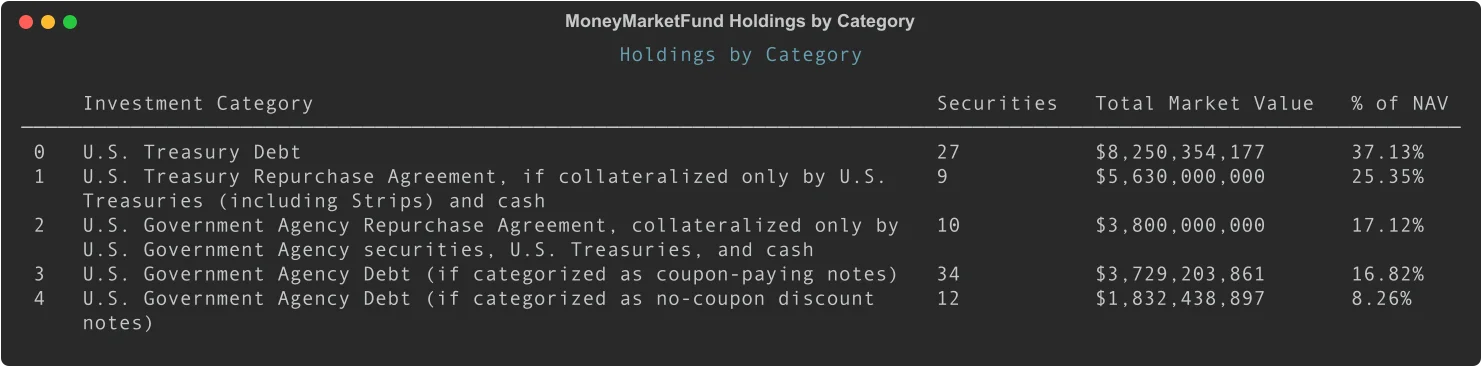

Holdings by Investment Category

Group holdings by SEC investment category to see asset class allocation:

mmf.holdings_by_category()

Returns a DataFrame with columns:

| Column | What it is |

|---|---|

category |

Investment category (e.g., "TreasuryDebt", "CommPaper") |

count |

Number of securities in this category |

total_market_value |

Sum of market values |

total_pct |

Percentage of fund NAV |

Sorted by total market value descending, making it easy to identify the fund's largest asset class exposures.

Look Up a Specific Fund

Search for a fund by the management company CIK or name:

from edgar import Company

# By management company name or CIK

vanguard = Company("VANGUARD")

filing = vanguard.get_filings(form="N-MFP3").latest(1)

mmf = filing.obj()

print(mmf.name) # Fund series name

print(mmf.report_date) # Reporting period end date

print(f"${mmf.net_assets:,.0f}") # Net assets

Or use the Fund class for a simpler path:

from edgar import Fund

fund = Fund("VMFXX")

mmf = fund.get_latest_report(form="N-MFP3")

The name property returns the full series name (e.g., "Vanguard Prime Money Market Fund"), and report_date shows the period end date.

Common Analysis Patterns

Weighted average maturity and credit quality

print(f"WAM: {mmf.average_maturity_wam} days")

print(f"WAL: {mmf.average_maturity_wal} days")

print(f"Fund category: {mmf.fund_category}")

Weighted Average Maturity (WAM) and Weighted Average Life (WAL) are key metrics for assessing interest rate sensitivity. Fund category indicates the type of money market fund (e.g., "Government", "Prime", "Tax-Exempt").

Top holdings concentration

holdings = mmf.portfolio_data()

# The pct_of_nav column already contains percentages

holdings[['issuer', 'title', 'market_value', 'pct_of_nav']].head(10)

# Or calculate manually if needed

import pandas as pd

holdings['market_value_float'] = holdings['market_value'].astype(float)

total = holdings['market_value_float'].sum()

holdings['weight_pct'] = (holdings['market_value_float'] / total * 100).round(2)

Treasury vs. agency vs. repo exposure

by_category = mmf.holdings_by_category()

treasury = by_category[by_category['category'] == 'TreasuryDebt']['total_pct'].sum()

agency = by_category[by_category['category'] == 'AgencyDebt']['total_pct'].sum()

repo = by_category[by_category['category'] == 'Repo']['total_pct'].sum()

print(f"Treasury: {treasury:.1f}%")

print(f"Agency: {agency:.1f}%")

print(f"Repo: {repo:.1f}%")

Liquidity buffer analysis

liq = mmf.liquidity_history()

if not liq.empty:

latest = liq.iloc[-1]

print(f"Daily liquid assets: {latest['pct_daily_liquid']:.1f}%")

print(f"Weekly liquid assets: {latest['pct_weekly_liquid']:.1f}%")

SEC rules require money market funds to maintain minimum liquidity levels. Daily liquid assets must be at least 10% of total assets, and weekly liquid assets must be at least 30%.

Metadata Quick Reference

| Property | Returns | Example |

|---|---|---|

name |

Fund series name | "Vanguard Prime Money Market Fund" |

report_date |

Reporting period end | "2024-10-31" |

fund_category |

Fund type | "Prime" |

net_assets |

Net assets (Decimal) | Decimal('26435168844.97') |

num_securities |

Number of holdings | 92 |

num_share_classes |

Number of share classes | 4 |

average_maturity_wam |

WAM in days | 45 |

average_maturity_wal |

WAL in days | 52 |

filing |

Source Filing object | Filing or None |

cik |

CIK of the filer | "0000102909" |

series_id |

SEC series ID | "S000004104" or None |

Methods Quick Reference

| Call | Returns | What it does |

|---|---|---|

mmf.portfolio_data() |

DataFrame |

All securities sorted by market value |

mmf.share_class_data() |

DataFrame |

Share class details and net assets |

mmf.yield_history() |

DataFrame |

7-day gross yield time series |

mmf.nav_history() |

DataFrame |

Daily NAV per share time series |

mmf.liquidity_history() |

DataFrame |

Daily/weekly liquid asset metrics |

mmf.collateral_data() |

DataFrame |

Repo collateral details flattened |

mmf.holdings_by_category() |

DataFrame |

Holdings grouped by investment category |

Things to Know

Values are in full dollars. Unlike 13F filings (which report in thousands), N-MFP market values are in actual USD. A market_value of 5,000,000,000 means exactly $5 billion.

N-MFP3 vs N-MFP2. N-MFP3 (June 2024+) includes daily time series with dates for the past 20 business days. N-MFP2 (2010–mid 2024) includes weekly Friday snapshots without explicit dates. EdgarTools parses both transparently.

Time series data. For N-MFP3, yield_history(), nav_history(), and liquidity_history() return DataFrames with 20 daily observations. For N-MFP2, they return weekly snapshots labeled "week_1" through "week_5".

Repo collateral. Repurchase agreements are a common money market fund investment. Use collateral_data() to analyze what securities back these repos. The has_repo column in portfolio_data() indicates which securities have collateral details.

Monthly filings, quarterly public disclosure. Funds file monthly, but only quarter-end filings are immediately public. Mid-quarter filings are released with a 60-day delay.

Share class structure. The same underlying portfolio may be divided into multiple share classes with different expense ratios and minimum investments. share_class_data() shows this structure.

WAM and WAL. Weighted Average Maturity (WAM) uses the next interest rate reset date for floating-rate securities. Weighted Average Life (WAL) uses final maturity. WAL is always ≥ WAM.

Related

- Fund Entities -- look up funds by ticker, navigate hierarchies

- Working with Filings -- general filing access patterns

- Fund Portfolios (N-PORT) -- mutual fund and ETF portfolio holdings